AI is not a trend

**AI is not a trend—it’s the new foundational layer of global innovation.”**

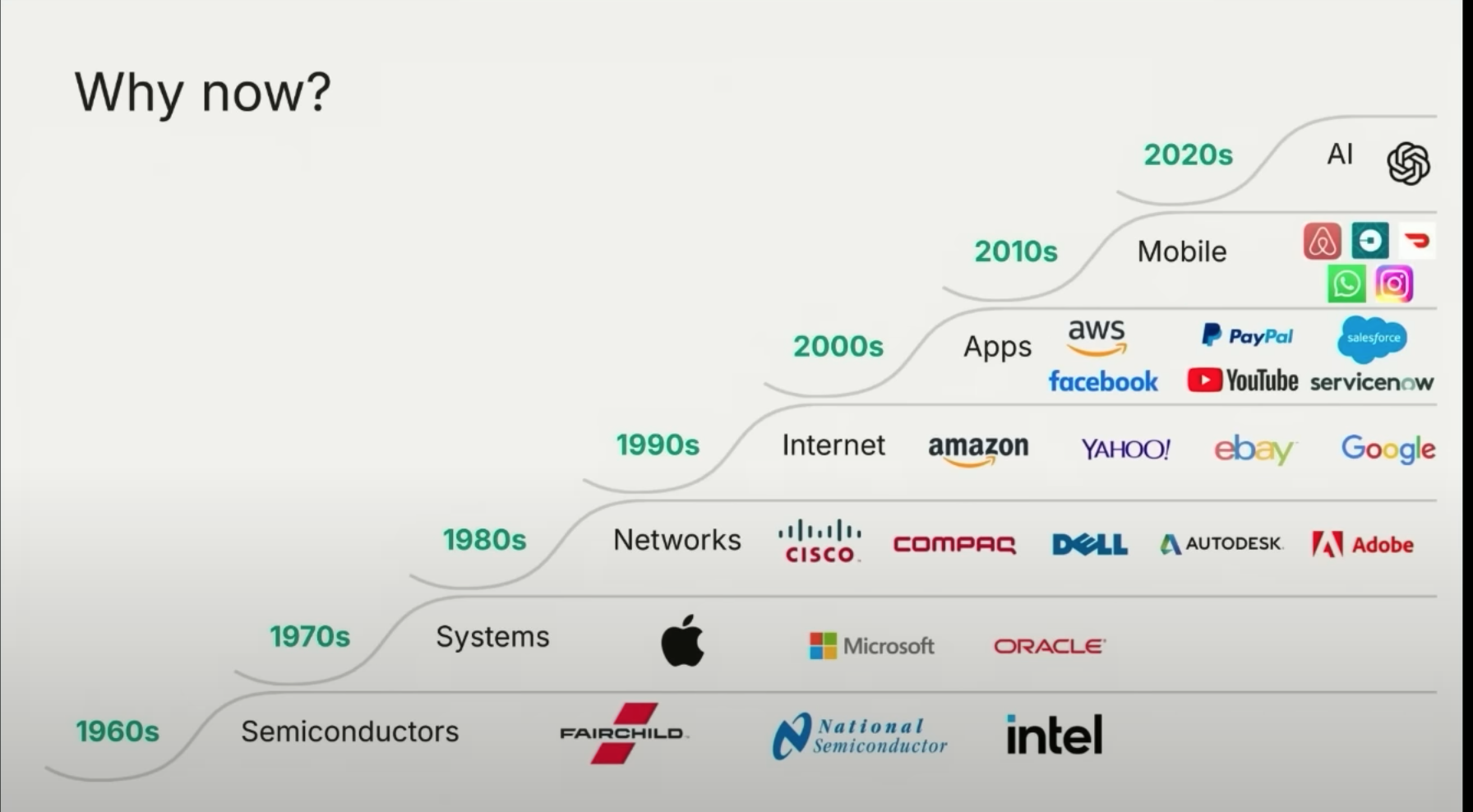

The timeline chart from Sequoia Capital illustrates the cyclical nature of technological innovation since the 1960s, highlighting dominant tech themes and associated market-leading companies in each era.

Key observations include:

1960s–1970s: Semiconductors & Systems

- Semiconductors (Intel, Fairchild) laid the hardware foundation for computing.

- Systems (Microsoft, Oracle) emerged as software and enterprise solutions gained prominence.

- Investment driver: Miniaturization of computing power and enterprise digitization.

1980s: Networks

- Networking infrastructure (Cisco, Compaq, Dell) enabled interconnected systems, driving productivity and globalization.

- Investment driver: Rise of client-server architectures and corporate IT spending.

1990s–2000s: Internet & Cloud

- Internet (Amazon, Google, Yahoo!) revolutionized commerce and information access.

- Cloud/SaaS (AWS, Salesforce, PayPal) democratized digital infrastructure and services.

- Investment driver: Scalability of web-based business models and subscription economies.

2010s: Mobile & Apps

- Mobile ecosystems (Facebook, YouTube, ServiceNow) transformed consumer behavior and enterprise workflows.

- Investment driver: Ubiquitous connectivity and app-driven monetization.

2020s: AI

- AI represents the next transformative wave, building on decades of accumulated data, compute power, and algorithmic breakthroughs.

- Investment driver: Automation, personalization, and decision-making at scale across industries.

Investment Recommendations

1. Focus on AI Ecosystem Leaders

- Core Infrastructure: Invest in companies providing AI hardware (e.g., semiconductor firms like NVIDIA and AMD) and cloud platforms (AWS, Microsoft Azure).

- AI-First Software: Target firms integrating generative AI, machine learning, and predictive analytics into workflows (e.g., ServiceNow, Adobe).

- Vertical Specialists: Identify sector-specific AI adopters in healthcare, finance, and logistics (e.g., AI-driven drug discovery or fraud detection platforms).

2. Diversify Across Maturity Stages

- Established Leaders: Allocate to mature tech giants (Microsoft, Google) with robust AI R&D budgets and ecosystem control.

- Emerging Innovators: Consider smaller-cap AI startups or ETFs focused on disruptive AI/ML technologies.

3. Monitor Regulatory and Ethical Risks

- Anticipate regulatory scrutiny on data privacy, AI ethics, and antitrust concerns. Companies with transparent governance frameworks will likely outperform.

4. Long-Term Horizon

- Historical patterns suggest AI-driven gains will compound over years, similar to past tech booms. Avoid overreacting to short-term volatility; prioritize firms with durable competitive moats.

5. Hedge Against Disruption

- Industries lagging in AI adoption (e.g., legacy manufacturing, traditional retail) may face existential risks. Underweight sectors resistant to AI integration.

Conclusion

The “Why Now?” chart underscores AI as the defining investment theme of the 2020s, mirroring the transformative potential of semiconductors in the 1960s or the internet in the 1990s. While risks such as valuation bubbles and regulatory hurdles persist, a strategic focus on AI infrastructure, applications, and ethical leaders offers compelling opportunities. Investors should position portfolios to capitalize on this cycle while maintaining vigilance for sector-specific disruptions.